By Jim Cline and Kate Kremer

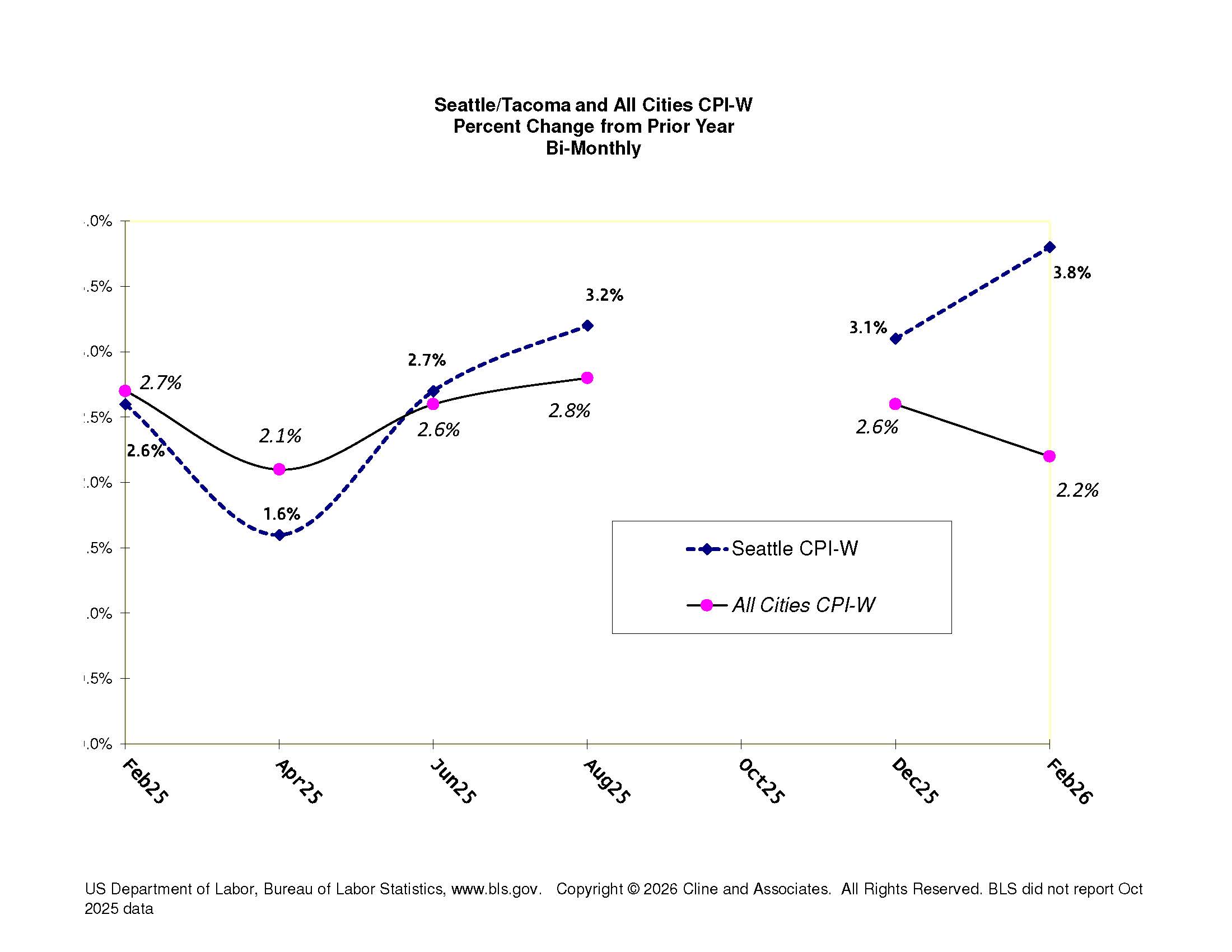

Last week the Bureau of Labor Statistics released their February inflation report with some interesting developments. Note that these numbers only measure inflation through the end of February and don’t include the likely increased inflation in March due to the spike in oil prices. The odd gap you see in the chart below is a product of the Fall Government shutdown with no October CPI report being released:

Last week the Bureau of Labor Statistics released their February inflation report with some interesting developments. Note that these numbers only measure inflation through the end of February and don’t include the likely increased inflation in March due to the spike in oil prices. The odd gap you see in the chart below is a product of the Fall Government shutdown with no October CPI report being released:

The declining inflation in the All-Cities numbers was not a surprise based on the various intervening economic reports. We had not anticipated this large jump in the Seattle numbers, though.

On a number of occasions, we’ve written on the general tendency of the Seattle numbers to outpace the National inflation. In some reporting periods, the numbers are closely aligned, in many periods the Seattle numbers are a bit above and on some occasions the Seattle numbers dip below. When we last discussed the situation in August 2o24 we stated:

Looking forwards, we are expecting the gap between these two numbers to continue to close further in the months ahead. If the national inflation trends continue their decline, as expected, to get closer to 2% over the next year or two, we would expect that Seattle would follow on that.

That doesn’t mean that the Seattle indices, at least over time, won’t ride a slight amount above the national numbers. As long as the Seattle regional economy continues to ride as strong as it has over the past several years, the related inflation pressures, especially on housing costs, will continue. The strong economy places demand pressures throughout the economy that simply and directly drives up prices for everything. We have said repeatedly that if you were to tie your contract to a particular index, the Seattle index is a better bet than the All Cities, and we continue to make that recommendation.

It remains the case that the Seattle Metro area economy is stronger than the national economy, pushing up all sorts of prices. More recently it appeared that Seattle Metro housing costs had been levelling leading us to believe that the National and Seattle indices would more closely converge. A closer review of the latest Seattle data, indicates that the inflation spike is driven by increased costs in a number of other areas besides, housing,

It should be noted that this BLS does not limit its range to the City of Seattle proper. While the BLS has sometimes broadened the index to cover the Metro area extending to Kitsap and Thurston Counties, currently BLS uses King, Pierce, and Snohomish County in its reported “Seattle” index. Despite that geographic location limit, contracts and negotiations throughout much of Western Washington and sometimes Eastern Washington cite to the Seattle inflation numbers.

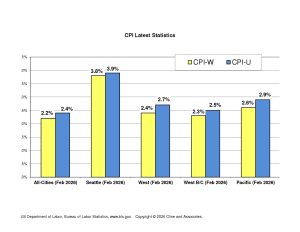

More recently we are seeing employers resisting the Seattle index and contracts now often incorporate the BLS “West” indices. The chart below shows the February inflation report for the West and other alternative indices:

Current and upcoming negotiations will be impacted by inflation developments which still remain unseen. An obvious pending unknown is the duration of the current Iran war and its ultimate short and intermediate impact on inflation numbers.

We are looking ahead to the June inflation report, but that won’t be known until mid-July. We’ve previously discussed the relative importance of the June indices and the extent to which they impact contract negotiations. The numbers are released as negotiations are often starting, and by common practice the June numbers are either incorporated into contracts or are used to create the floor for negotiated wage increases. While it’s clear that many Washington public safety contracts over the past few years relied on “settlement trends” that surpassed CPI, there’s no doubt that existing inflation trends are a pivotal factor in contract negotiations.

We’re all seeing the headlines reporting a spike in oil prices. While a trip to the gas pump provides some immediate sign of inflation, the inflation impacts of these oil price increases are more impactful than just the price of gas. The whole category of CPI “energy” prices will be going up but also most products purchased whether it’s food that is consumed (after being produced using petroleum-based fertilizer) or goods that are transported, impacted by rising oil prices.

We have not seen reliable predictions yet that look as far out as June but at this point, we’re anticipating the likelihood that the All-Cities index will surpass 3% and that the Seattle index (if it continues on its recent trajectory) will exceed 4%. The main condition we see now is uncertainty, and we cannot give much weight to any pending predictions until that uncertainty is reduced.